When all is said and done, the RBA can do 3 things this Tuesday.

- It can raise rates.

- This can leave rates alone.

- It can knock them down.

The last one is the easiest to rule out.

Advertisement

In February, the RBA told us correctly, that inflation was running hotter than they would have liked and that a rate hike was needed to ease pressures. Since then, petrol prices have risen by about 70 cents per liter in most parts of the country, while diesel prices have risen even more.

We can be sure that day after night this increase is already being reflected in fruit and vegetable prices this week, followed closely by meat, and everything else in short order.

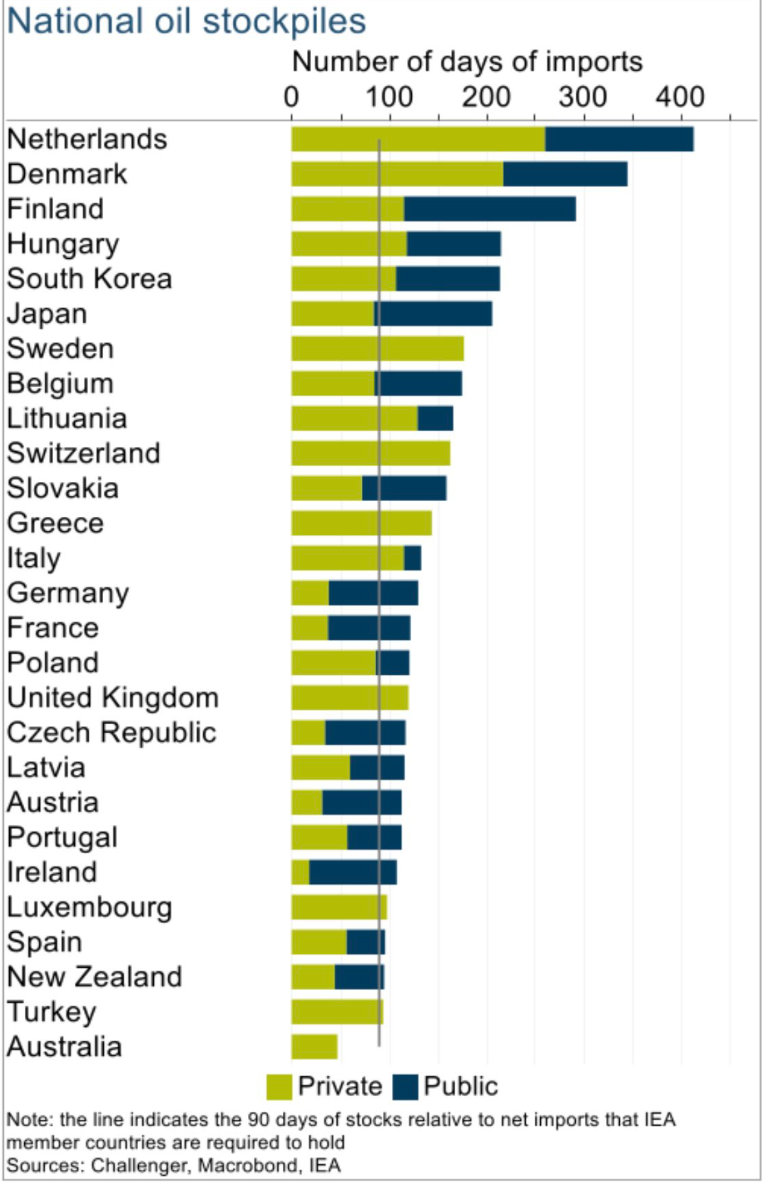

The price hike comes despite the government amending rules to ensure retailers don’t hike prices. This raises the possibility that this is not a price hike due to rising prices, but the simple fact that in a nation that has around 30-35 days worth of fuel storage capacity – one of the lowest in the developed world – people are worried about being able to fill their tanks at any cost in the near future.

Advertisement

Despite regular warnings from politicians and bureaucrats about ‘panic buying’ there are as many mega four-wheel drive utes on the road as Australia, and with fuel reserves as scarce as Australia is now, the urge to top up the fuel is common sense for most people.

The fact that our politicians and bureaucrats cannot recognize this exposes the gulf between them and the national interest as perceived by the electorate.

Returning to the options facing the RBA, the notion of leaving rates alone is next in line. These are almost certainly the hopes of politicians.

Advertisement

To get here, the RBA will need to reflect on what it has done with the single rate hike it has now plunged into the fray with rising fuel prices, killing the outlook.

The RBA knows, as politicians and bureaucrats do, that the inflationary pressure is not in the spending propensity of the individual consumer, but in the aggregate consumption of a population that is being fed by huge amounts of forced immigration.

This pressure is coupled with non-tradable inflation. It is inflationary pressure that is largely baked in. Rent, electricity bills and rates, car registration and education expenses, insurance premiums, and of course commuting expenses. which people cannot avoid easily.

Advertisement

Everyone knows, and the RBA knew before the February hike, that such spending has put pressure on Australian inflation and that the February rate hike will have only a marginal impact on such inflation.

They may consider that a 30% increase in fuel prices would have a similar effect in curbing trade inflationary pressures. People on the road are less likely to spend more on anything other than fuel and are likely to be cutting back on discretionary spending to offset the extra fuel costs.

The only other illusion that could enable an RBA hold is the psychedelic idea that as soon as the Iranians buckle, prices will return to where they were five weeks ago.

Advertisement

But for the here and now, prices are almost certainly going to follow the rise in fuel prices, and an RBA hold would give rise to the possibility of a loss of grip on inflation and possibly another rise in house prices as ‘investors’ or investors realize that there is nothing else going on in the local investment road targeting consumers.

This gives us an idea that there will be a rate hike on Tuesday. At this point, there must certainly be a question about the appropriate size, given that rising fuel costs are going to be a very significant inflationary pressure, and the RBA will know that a rate hike in February is unlikely given the massive non-discretionary inflation Australia has experienced.

From there comes the idea that a 30 percent increase in fuel prices could require a 50 basis point increase. This is likely to lead to protests and a tendency for the government to point the finger at the RBA for taking ownership of the decision.

Advertisement

In fact, 50 basis points could be enough to push a large number of stressed mortgage payers to the breaking point. Considerable evidence indicates that most voters are in a stressful situation with regard to rent or mortgage.

It makes us all wonder if windsurfing has an economic impact. This situation is exacerbated by a heavily indebted economy that relies heavily on exports of lightly taxed commodities, with many believing that swapping housing at ever-increasing prices is a viable economic model.

At this sad juncture there are many other considerations which lead us to the predicament in which we are now.

Advertisement

The first background is that, in 2008 and again in 2020, when crises threatened to engulf the global economy, central banks around the world responded by pumping in cash. Funding windows, swap lines, investment incentives, and direct financial incentives.

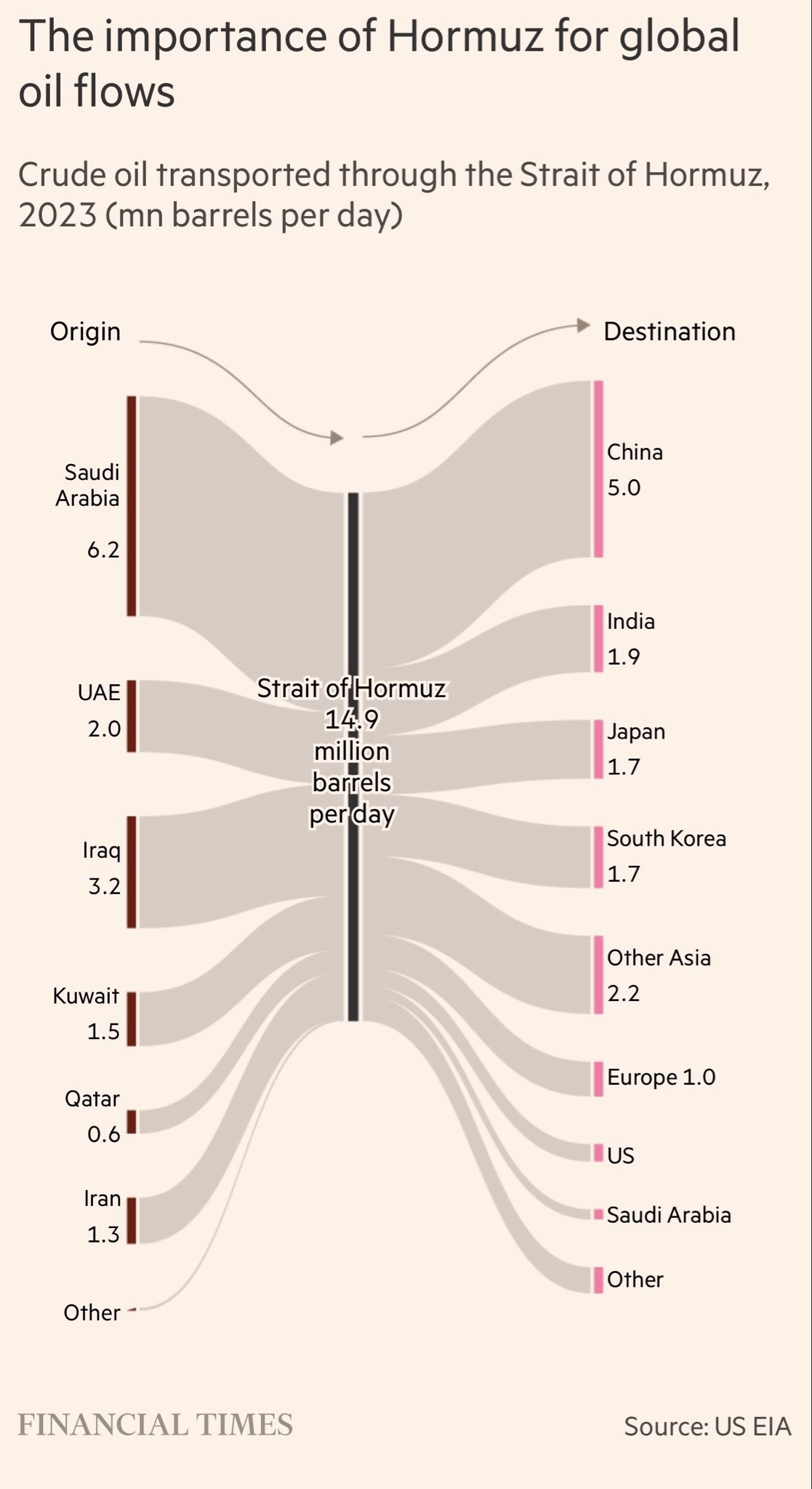

After two weeks of fighting Iran and halting the flow of crude oil through the Strait of Hormuz, it is clear that global markets are facing a similar trend.

We also know that last week, many countries with capacity did so, prompting an emergency release of global fuel reserves. At that point, the question becomes whether, in deliberating on coordinated action to support fuel availability, the question arises, ‘So if it doesn’t work, it will be coordinated fiscal stimulus again, yes?’

Advertisement

From there, looking at the developed world, it appears that the US is not far from a debt ceiling crisis, the EU is committed to considerable fiscal stability in an economy already reeling from energy shocks from Russia and Ukraine, a China now facing a demographic crisis and a hole in the financial system, a Japan that has bathed in bonds for a generation and an Australia with the highest levels of government.

This may be in line with the views of US President Trump, who would no doubt like to open the door to spending but treat the future people of the developed world like the scoundrels he refers to as the Iranian leadership.

Advertisement

Even when crude oil prices were falling, Australia couldn’t get it right, and that’s largely because we stopped producing and refining our own and became price takers for others.

Now we are all crooks.

But those of us waiting for the RBA’s decision this week will note that we’re all grumpy now.

Advertisement

The RBA could essentially raise rates and treat mortgage- and rent-stressed Australians as scumbags through its servicing requirements, or leave rates unchanged and treat future Australians like crooks through inflation or possibly higher home ownership costs.

Maybe we’ll wait for the world’s fiscal stimulus to unfold and point out that others are worse off than we are.

More cynicism comes from both sides of mainstream politics and bureaucracy. It has deindustrialized Australia so much that we earn very little of what we consume. We traded that for commodity receipts, which we allow producers to eliminate or leave the commodity untouched, as a commodity-dependent economy if it wanted to convince its people that it was a developed economy.

Advertisement

Globally, it seems that our fate is in the hands of the administration of America and Israel. They may have a valid point when they say that the Iranian leadership is made up of dishonest people.

But OPEC clearly established 50 years ago that the developed world is heavily dependent on energy passing through the Strait of Hormuz. Those running the US and Israel chose to attack Iran without telling the rest of the developed world that their energy lifelines were about to be threatened.

Likewise, they apparently haven’t given enough thought to the idea that Iran, as it has made clear countless times, would threaten energy flows through the strait it sits on. The peoples of Asia, Europe, Japan, and Australia, who depend on these energy flows, may assume that those on the warpath, unconcerned with the consequences of their course, have a sense of mistrust about them as well.

Advertisement

The Chinese decision to immediately stop aviation fuel exports should highlight the flaws in our decision-making leading up to this point. Is anyone going to warn them that they may feel ‘sovereignty risk’ about investing there?

One of the benefits for Australians may be that, from here, we can tell the gas cartel where to get off and start making energy policy for Australians rather than avoiding a global capital tax, especially given that China is a buyer of our gas.

And once we start thinking that, we need to start thinking about bringing meaningful productivity back to this country, rather than being rude to future Australians and immigrants, expecting their lives to improve by being enslaved by unproductive debt.

Advertisement