Australian house prices have risen strongly for almost 30 years, barring a few minor hiccups along the way.

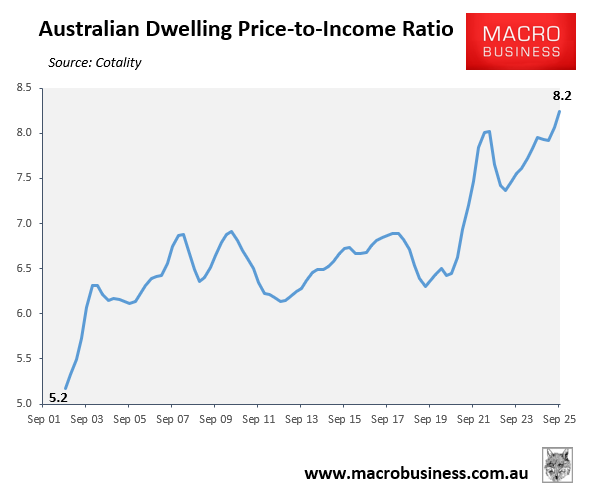

According to Cotality, this explosive growth means that at the end of 2025, house prices were at a record high relative to household income.

Advertisement

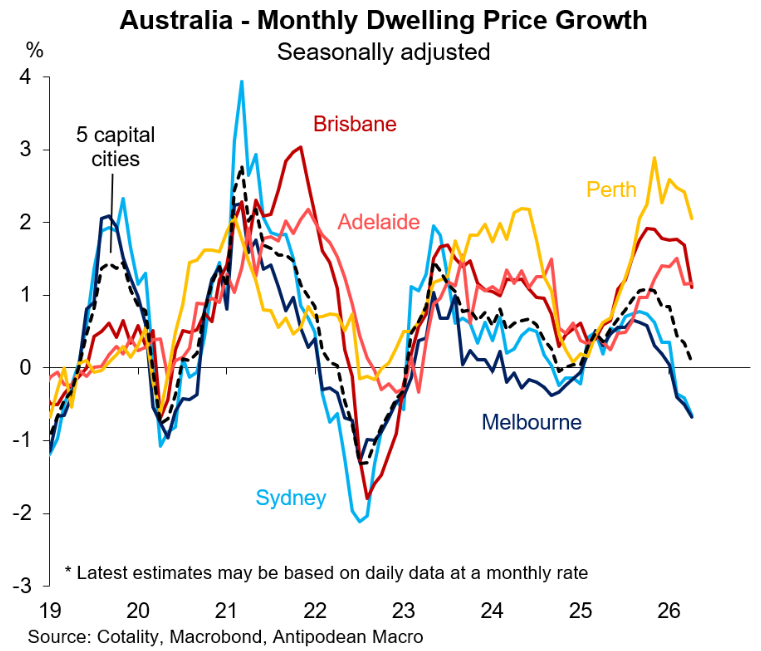

House prices in Australia’s capital cities are falling sharply after the Reserve Bank of Australia’s back-to-back rate hikes, led by Melbourne and Sydney:

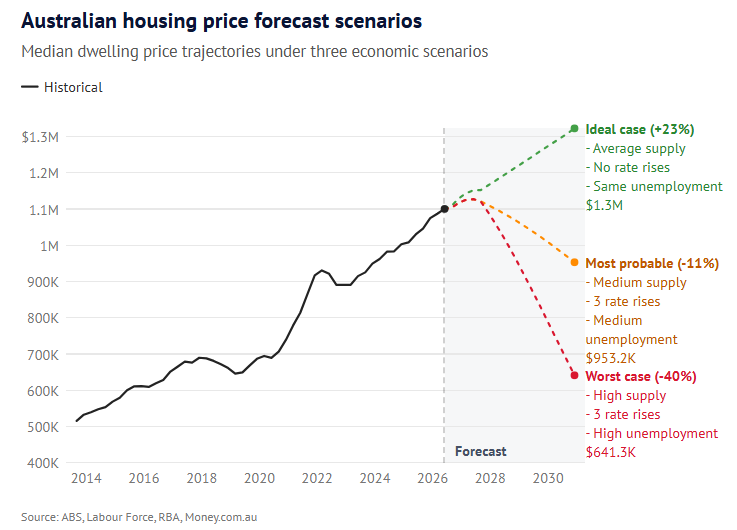

With at least two more rate rises in financial markets this year, along with pending changes to property tax concessions and a weakening economy, new modeling by Money.com.au commissioned by Primera Research suggests housing prices could fall by as much as 40 per cent by 2030:

Advertisement

According to Premara’s “most likely” scenario, Australia’s national average housing value would rise by about 4.9 per cent from December 2025 to $1,127,000 by June next year, but then fall 15.4 per cent from that peak to $953,000 by the end of 2030.

Premara’s worst-case scenario, which includes three rate increases, unemployment, and an oversupply of housing, suggests that home prices could drop nearly 40 percent from a peak of $1.1 million to $641,300 by December 2030.

Advertisement

On the other hand, if the RBA does not raise rates further, unemployment were to remain stable, and supply remains constrained, house prices could rise by 23% by the end of 2030, reaching $1.3 million.

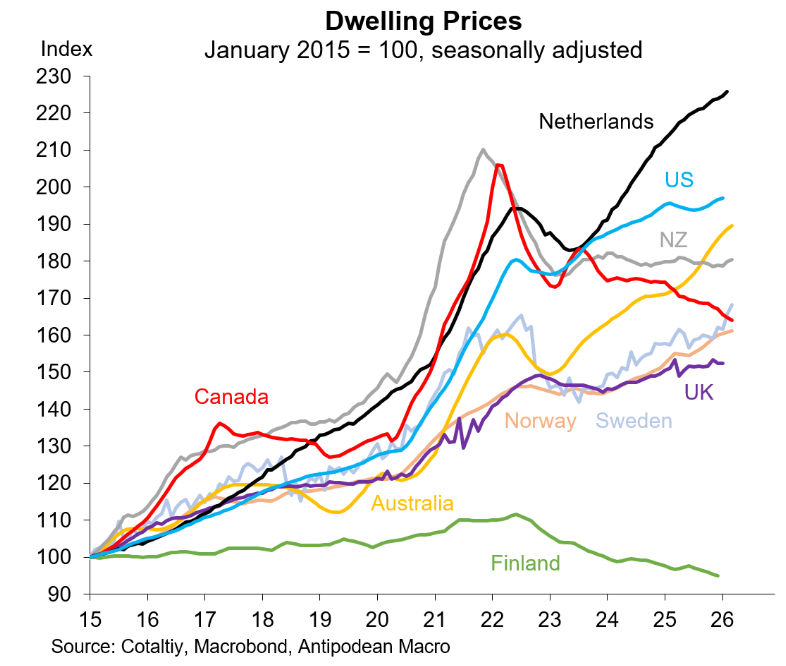

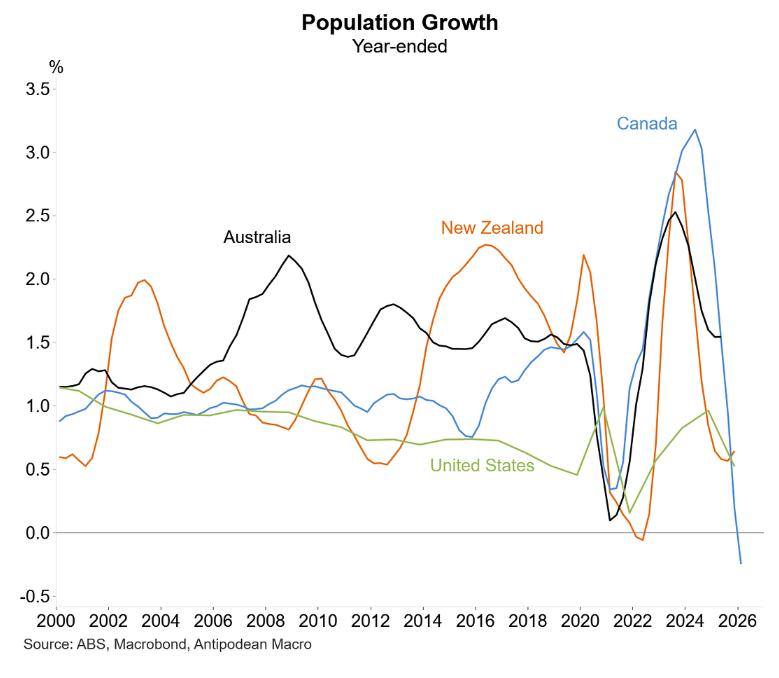

It’s important to remember that two of Australia’s most similar economies — New Zealand and Canada — have experienced large house price declines, as illustrated by Justin Fabo from Antipodean Macro below.

Advertisement

Both markets are down about 20% from their most recent peaks.

If Australia’s two most similar housing markets can experience severe house price declines, why can’t Australia?

If the RBA raises rates further and the economy weakens, ‘fear of missing out’ could easily turn into ‘fear of overpaying’ as a result of reduced mortgage affordability and borrowing capacity, or a significant rise in unemployment.

Advertisement

This will lead to a significant reduction in demand and a sharp adjustment in prices.

However, the most notable difference between Australia, New Zealand and Canada is that Australia has historically had high levels of immigration, supporting demand through population growth. In contrast, population growth has fallen significantly in the other two countries (and turned negative in Canada).

Advertisement

As a result, Australia’s housing market is structurally undersupplied, while Canada and New Zealand are oversupplied.

Nevertheless, I would be very cautious about leveraging to invest in Australian property. At some point, gravity will take over.