The story of February was a surging Australian dollar amid forecasts of incredible profit growth. Profit forecasts strengthened throughout the month, helping to lift share prices, but for Australian investors, the rising AUD offsets all those gains. The key question in March is whether profit growth (15%+ forecast for each of the next two years) will remain unconvincing or will not be credible due to rising energy costs.

Q1 reporting by companies only highlighted the strength of company earnings undercutting the market. Although many countries have economic problems, they are mostly affecting consumers and workers – companies (what?) are doing very well.

Advertisement

Trump TACO: Why markets are holding their breath betting on a deal

If you can ignore the smoke billowing from the Middle East for a moment, the fundamental backdrop for global equities is actually… pretty good.

A weak(ish) consumer and cooling inflation point the way to lower interest rates (except in Australia). At the same time, income is booming. AI-powered capital expenditures are making the dotcom capex boom blush. Toss in a deregulatory tailwind and massive government deficits, and you have a recipe for consistently high margins. But that “if” is doing a lot of the heavy lifting.

Enter “TRUMP TACO”.

is the current base case of the market. TRUMP TACO (TRump Ohalways CHook Ohut) In this scenario, President Trump follows his “deal maker” persona. He declares a symbolic victory, negotiates a deal — perhaps one that favors enriching certain power brokers or Iranian generals in exchange for reopening the Strait of Hormuz — and walks away from an all-out Iran war. If TACO is offered, the positive economic setup continues, and markets are likely to rally.

Advertisement

The relevance of hope

The problem? The distribution of results is not a neat bell curve. It’s a rock.

- upside down: Limited If a deal is reached, we mostly just get back the “normal” growth we already expected.

- Cons: The extreme lies at the other end of the spectrum. $200+ oil and a deep, structural global recession as energy supply chains are physically disrupted.

Currently, the market sees TACO as a foregone conclusion. We disagree. Uncertainty remains at a decades-old high, and history suggests that a “deal” usually requires a catalyst of pain. Will Trump move to end the conflict because he wants to, or because the crashing stock market and $6-a-gallon gas are forcing his hand?

The Minsky Trap: Why Stability Is the Enemy of the Deal

However, there is one Minsky-esque irony Here was Hyman Minsky’s main insight at play. Stability is unstable. In this context, the higher the “prices” in the Trump axis, the more stable the market remains. And the more stable the market remains, the less pressure Trump will actually have to pivot. If the S&P 500 stays near record highs, Trump is “allowed” to stay the course. To get TACO, we likely need a catalyst of pain — a market disruption deep enough to threaten its narrative of economic dominance. Without a falling stock market or ever-increasing increases in gasoline crushing voters, it’s more likely to double. It is the belief that he will save the market that prevents him from doing so.

Why are we sitting on 20% cash?

Because of this “Minsky Trap”, we have decided to catch it deliberately. 20% more cash From our usual mandate. In a market with relatively high valuations and an asymmetric risk profile (limited upside vs $200 oil clifftop), “discretionary” is actually our most valuable asset. This cash plays two roles:

- Safety Net: If the “Trump TACO” fails to materialize and we descend into a deep regional war and global recession, this cash buffers our downside.

- “Call Option”: If Trump does Eventually pivot—likely after a period of market-clearing volatility—we’ll have dry powder to buy the wreckage and fuel a TACO-fueled recovery.

At current price levels, the cost of being slightly “underinvested” is minimal compared to the cost of being fully exposed to a risk event at once.

Advertisement

Where is the shelter?

In a world of extreme uncertainty, “obvious” hedges often lead to hidden traps.

- Oil and Gas: A Paralympic Victory? You think energy has a hiding place. But the outbreak of the Ukraine war saw Europe and China move away from foreign fossil fuels. This crisis will redouble those efforts. You might get a couple of months (or two years) of extraordinary profits, but you might also knock 10 years off the terminal life of the industry as the transition to local renewables and nuclear goes into hyperdrive.

- The “America First” export trap: Do you want US oil stocks? If oil hits $200, does a populist Trump administration continue to allow record exports while American voters suffer? A “national security” cap on exports would keep U.S. prices low for voters, but would hurt “jumbo” profits for the companies you bought to hedge against.

- Uranium: People talk about a nuclear renaissance, but buying fuel for plants that won’t come online for 15 years is a “forever” bet with the risk of mass execution. Matching the timing with the 2026 energy crisis is a tricky trade-off.

Stock Focus: The Infrastructure of Change

We will continue to support Electricity Services Sector. Whatever happens—whether China builds more coal/solar or Europe pivots to more nuclear/wind—the global grid needs to be rebuilt, plugged in, and repaired.

Advertisement

We are buying the “plumbing” of energy transfer, which is essential regardless of controlling the Strait of Hormuz. Schneider, ABB, Hitachi, Vestas Wind and Wartsila are the main parts of this part of our portfolio.

We have also recently topped a number of healthcare stocks (including GSK, Pfizer and IQVIA), topped our defense stocks, particularly in Europe, and have been buying into software stocks.

Advertisement

Capital deployment

In a market that is pricing in TACO but looking at a potential $200 oil shock, cash isn’t “trash” – it’s an option.

- If the Trump Taco comes: We deploy cash in a comfortable, growing market.

- If the dispute escalates: We have dry powder to buy debris.

Bottom line: We are not betting against any deal. We simply refuse to pay it as if it were a sure thing. We are preparing the cash for when the “Minsky trap” finally breaks.

Distribution of assets

Advertisement

We were slightly underweight in shares overall, significantly underweight in Australian shares. In early March, we sold a lot of stocks. We are market-weighted bonds, with little foreign currency:

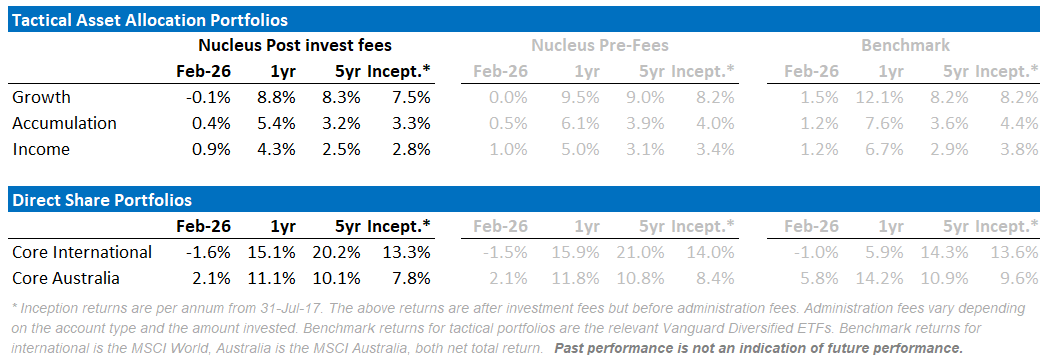

Performance Description

Advertisement

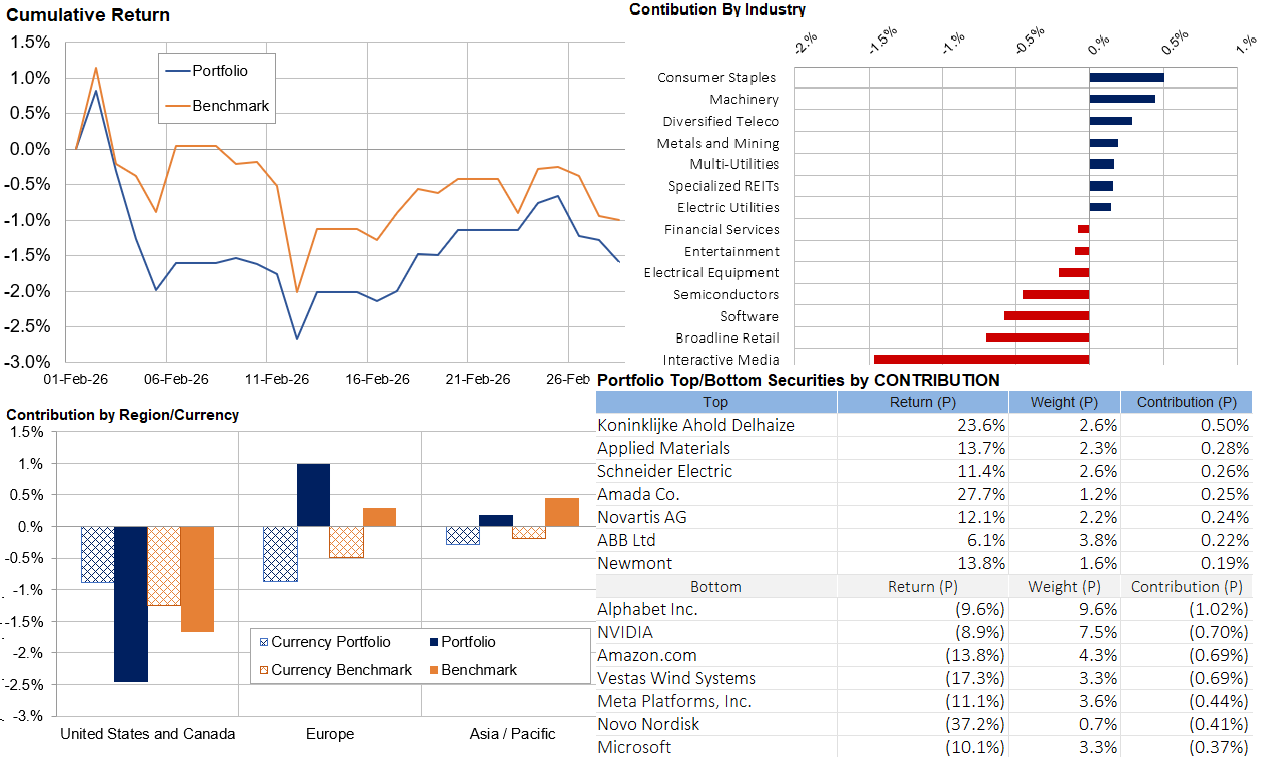

Core International performance

Advertisement

February saw a decline in stocks, particularly in the US, with more defensive stocks outperforming, particularly in Europe. The currency was a drag on the performance of all currencies as the $A strengthened.

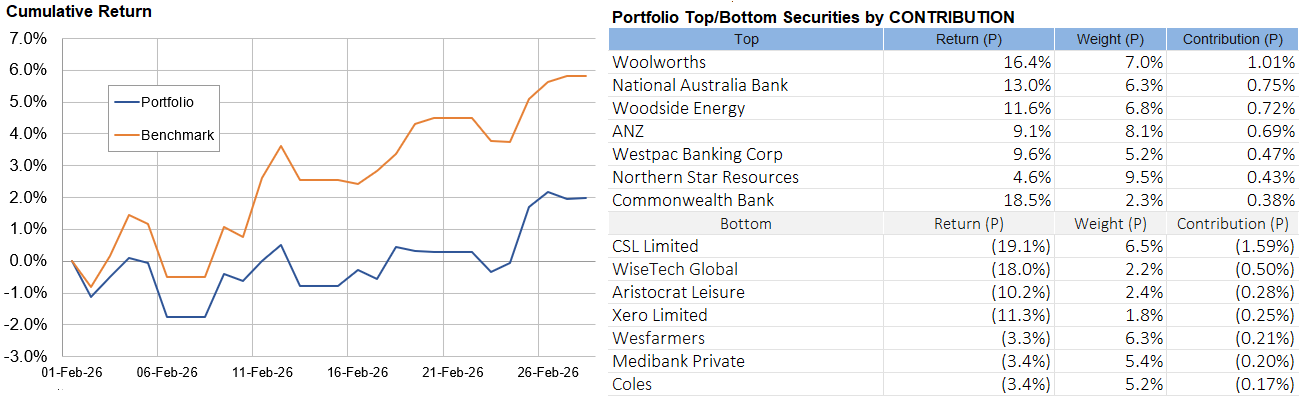

Core Australia performance

Advertisement

Growth stocks lagged behind the outperformance of banks and resource stocks.

Damian Klaasen is Chief Investment Officer at the Macro Business Fund, which is run by Nucleus Wealth.

Advertisement

Follow up. @DamienKlassen But X(Twitter) Or LinkedIn

The information in this blog contains general information and may not take into account your personal goals, financial situation or needs. Past performance is not indicative of future performance. Damian Klassen is an authorized representative of Nucleus Advice Pty Ltd, Australian Financial Services Licensee 515796. And Nucleus Wealth is the corporate authorized representative of Nucleus Advice Pty Ltd.